All About The Budget

It’s been way too long since we met like this. It’s funny how a whole year can get away from you. It definitely had something to do with our middle child getting married. I feel like my whole life was just one big wedding planning event last year. I felt a sense of accomplishment when I managed to get my Word Wednesday posts sent out.

With a new year, begins new focus (and no more weddings any time soon). For this first edition of Finance Friday 2026, I want to dig deeper into the world of budgeting.

If you haven’t read my previous Finance Friday post from last year, where I break out some basic money habits, make sure to click below and check that out!

Click the picture to read “Let’s Talk Numbers”

Budget

Most people view this word as dirty, and something not be uttered in the home. As long as the bills are paid, food is on the table, gas is in the vehicles and we can go do some fun things every now and then, life is good. Why do I need a budget?

Welcome to the “living pay check to pay check” culture. This mindset is the reason so many people are stressed out over finances and wonder where all their money went before they get paid again. One week you have plenty of cash flow, and the next you are at the Urgent Care with a sick kiddo who needs copayments and medicine, and suddenly you are maxing out another credit card. Budgeting is vital for proper money management, and cuts down on financial stress.

Let me use my most recent large, scale event as an example. If I didn’t have a detailed budget laid out for all expenses for our daughter’s wedding, it would have been very easy to overspend, and then I would be stressed out when the money was short to pay for all the necessary items.

Don’t be fooled. Running your monthly household is just as complex, and just as easy to blow the finances, if you are not tracking where your money is going.

Enough chatter…. let’s get going with practical application.

List the Details

First, you will need to calculate what your monthly net income will be. (Net income is the amount you actually receive after all taxes, health benefit premiums, retirement, etc.. come out. In other words, the amount that actually hits your bank account each pay date). If you are an hourly worker, take a look back over 3 months worth of pay statements and average those amounts. That number is a great place to start when determining how much you are able to bring home each month.

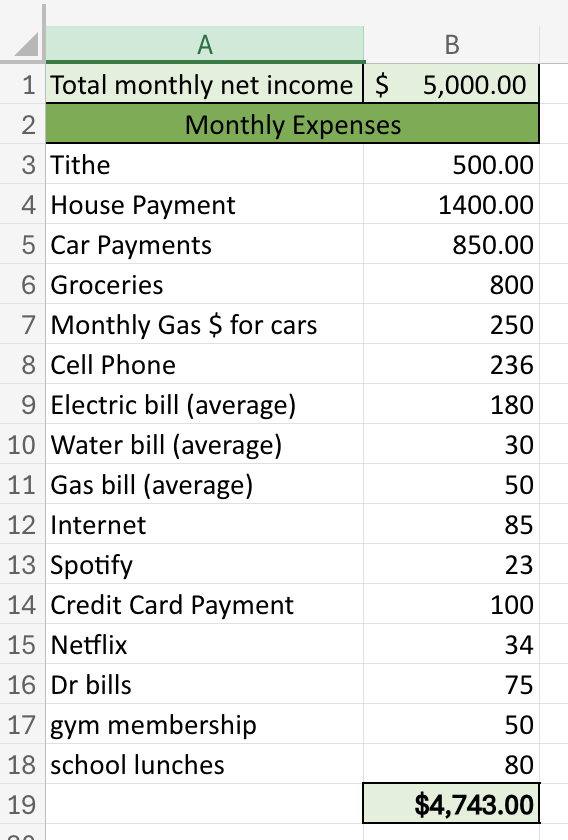

Next, you are going to begin listing out all of your monthly expenses and their amounts. I have attached an example spreadsheet for your review below. (*Please note: any of these steps can be completed using good, ole’ notebook paper, pen and calculator. Especially if the thought of trying to use Excel gives you hives.)

You will note, I have everything detailed out in one column (A), with the amount of that bill in the column (B) beside it. This is called a “line item” on your budget sheet. Try to account for every monthly expense, including those sometimes overlooked items like haircuts. Once everything is listed out, total your amount column (in our example this is column B) so you can see how much it takes for the basic, financial needs of your household.

A couple quick Excel tips:

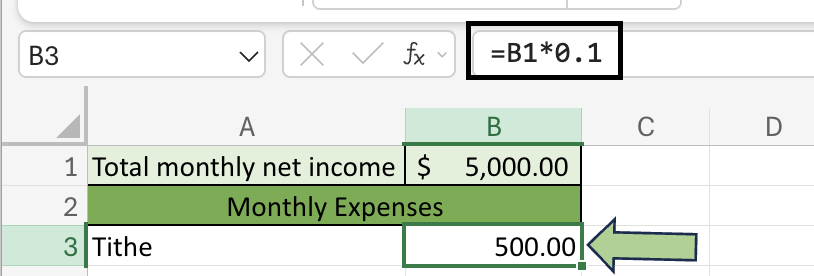

Tithe Formula

To have your sheet calculate your tithe automatically, click the cell beside the tithe line item. (In our example, this is cell B3) Type the “=” sign so you can begin a formula. Next you will click on the cell that has your monthly net amount. (In our example, this is cell B1) Then type a “ * “ sign (this is multiplication in Excel). Finally, enter whatever percentage value you want to tithe in decimal format and hit enter. For example: If I tithe 10% of my net income, the formula in cell B3 will look like this: =B1*0.10 This will give you the automatic calculation. Any time you change your monthly net amount, it will update your tithe number for you.

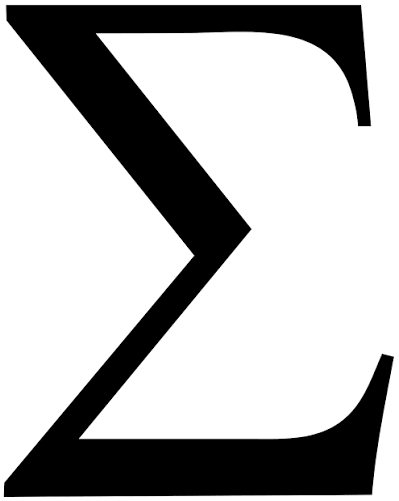

Excel AutoSum

If you click the cell under the very last expense line item amount (in our example above, this is cell B19) and click “AutoSum” in your task bar at the top, this will automatically sum your column for you. The symbol I have to the left, is what you are looking for.

Begin the Planning

Now that you can easily see where the bulk of your finances are going, let’s start to dig deeper into planning. It is always best practice to pay ahead on your bills. Here is what I mean by that.

Most people are paid on a biweekly basis, so we will use that pay cycle for our illustration. (Adjust where necessary if this is not the case for yourself). If you live off of two incomes, and are not paid on the same weeks, set up your payment cycle by the week of the person who brings home the higher net amount. Now, let’s set up the scenario.

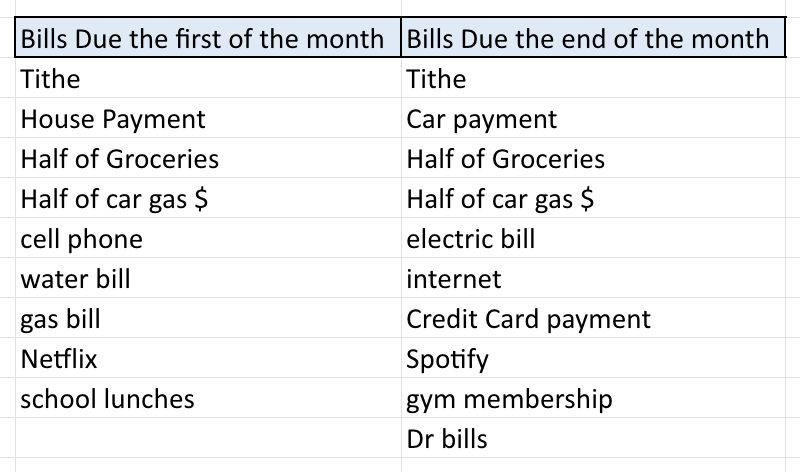

Tom Smith and his wife Judy, are planning their bills for the upcoming month of February. Tom brings home a higher net wage than Judy, so they plan to pay bills on each Friday Tom is paid. In the month of February, Tom will be paid on the 6th and the 20th.

They have some payments due the first to middle of the month and others that are due the middle to end of the month. Tom would like to always stay ahead on the bills, so they split the bills as such:

To understand how Tom and Judy stay ahead on their payments, we need to go back to January and the second pay check of the month for both of them. Judy was paid on January 16th. They spend no money from Judy’s check, so they can wait and plan the next Friday when Tom is paid, since he brings home the greater amount. Tom received his pay check on January 23rd.

On Friday, January 23rd, Tom and Judy looked at their list of bills and wrote out everything that was going to be due February 1st-15th. They totaled that amount, and began paying all of these bills immediately on the January 23rd date. They realized the water bill and gas bill had not come in yet, as it was still too early to receive the February billing statement, so they made a note to keep those line item amounts reserved in the bank account, for when the bill came in. This assured the money would be available to pay the bill promptly upon receipt.

After paying all of February’s first of the month bills (and calculating the reserve money for bills not yet received), Tom and Judy realized money was going to be a little tight for the next two weeks until Tom was paid again on February 6th.

They always made a practice of keeping back $50.00 emergency money in case unexpected items popped up between pay dates. After planning for emergency money, this only left $100 to get them through the next two weeks. (*Note: Yes, Judy will be paid again the following week, but don’t be tempted to spend money you have not budgeted yet. This is how overspending occurs. Tom and Judy pretend they get paid on the same Friday, and ignore the money that is deposited from Judy’s work. They stick to the budget and stay on track! Now back to the story…)

Tom and Judy decided together, they would not got out to eat or do any extra spending, no matter how small, until the next pay date. This would help keep their finances in good shape, and would reduce the risk of having to use the credit card- which they were working very hard to pay off.

Having a solid plan in place, they felt at peace, even though money was snug. Five days later, their youngest daughter got an ear infection, needed to see the doctor and was placed on antibiotics. After a $25.00 copay and $10.00 Amoxicillan fee, they were still in good shape. Three more days passed, and big brother also ended up at the doctor due to a sinus infection. Between the copay and two prescriptions, they were out another $55.00, but still holding financially strong, since they had stuck to their plan and not hit any restaurants in a moment of weakness.

Finally, pay day came. Sitting down together, they combined their net amounts from Judy’s January 30th check and Tom’s February 6th check. Looking at their detailed list, they wrote out all the bills that were due February 16th-end of the month. Once again, they paid all of these bills immediately, or planned money in reserve for bills not yet received, but would come. This means, by the first pay check of February, Tom and Judy have now paid and/or have money in reserve for every bill in February. This removes a large amount of stress from their minds.

This time after taking out their $50.00 emergency money, and paying extra on the credit card to get it paid down faster, they had $275.00 left over to last for the next two weeks. They set aside $100.00 for eat out money, $25.00 for a birthday present for their son’s friend, and $50.00 for a new pair of shoes for the middle child that will not stop growing.

Two weeks pass, and thankfully no emergencies arose. Tom was able to pick up a little overtime, so when the February 20th pay date rolled around, after paying all the bills that were due March 1st-15th and budgeting their emergency money, they still had $350.00 extra to live on the next two weeks.

Putting It All Together

Do you see how planning your every dollar matters and helps you make wise decisions about how to spend your money in-between pay dates? The scenario with Tom and Judy is real life. Kids get sick, grow out of shoes or forgot to tell you about the book fee they have that is months past due. Nails somehow find their way into tires or the battery on the lawn mower dies. There is always something that seems to pop up.

Now, let’s say the way your bills fall due during the month, creates a lopsided amount of money, where you don’t have enough to cover everything from one pay check. For example: Your first check of the month net is $2,500, but your house payment and both car payments are due, plus some other bills. Your bill total is $2700 for that pay date. However, the opposite is true for the end of the month bills that are due. There are less of them, and so you end up with a large amount of extra money after paying bills from your second check of the month.

What you would then want to do, is split your house payment and car payment, to help balance out the cash flow. Here is what I mean:

You will be paying the rent/mortgage and cars on the second pay date of the month, because they are due the first of the next month.

On your budget sheet, when planning what bills will be paid with what check, you will list half the house & car amounts for the first check, and the other half for the second check.

You will be setting this money in “reserve” like you do for bills that haven’t come in yet, and pretend it doesn’t exist.

Let’s say the house payment is $1400 and the cars are $850. On the first pay check of the month, you will place in reserve $700 for the house and $425 for the cars.

When the second pay date rolls around, you have not touched the reserve money, so now you only need an additional $700 to make the house payment and an additional $425 to make the car payments.

Spread the money out, so it’s more balanced and doesn’t leave you broke one pay date and overflowing the next.

Detailed planning helps keep you from overspending and going into debt by using credit cards or taking out loans. On our next Finance Friday post, we will go more in depth about debt and how to dig your way out of the money pit.

Until then, I encourage you to sit down with your significant other (if a married couple) and get a game plan. If you are single, do the same! There is power and peace, in knowing where your pay check is going. It is also being a wise steward of the resources given to us by God the Father. We are to handle them well.

Yes, this may mean you cannot make your daily Starbucks run, go out to eat with your friends after church next week or buy that cute pair of earrings. It does take discipline and self control to handle your spending. This is where your path to financial freedom starts.

Money, most of the time, is not a math problem,

it’s a MINDSET problem.

When I decided I wanted to simplify my life, and focus on the things that truly matter, it started first with my relationship with Christ and then our finances. I have lived stressed out and stretched thin, playing the “more month at the end of the money” game. I understand what it feels like to not have enough to make ends meet.

I am also here to tell you, there is hope and there is freedom from your money woes! I’m excited to see how God will transform your life, when you take the simple step of obedience in managing your money well. Please reach out to me if you have any, more in-depth questions you would like answered regarding setting up a budget. Drop your question in the comments, or send me an email from my contact page. Let’s tackle this together and Live Beautifully Simple with our finances in 2026!

“In the house of the wise are stores of choice food and oil, but a foolish man devours all he has.” (Proverbs 21:20)